How Elizabeth Warren incited the banking crisis of 2023.

Last night I had the pleasure of sitting down with Caitlin Long, Founder and CEO of Custodia - a fully reserved bank providing banking services to bitcoin companies, to discuss an affidavit written by Elaine Hetrick of Silvergate Bank. Elaine is the Chief Administrative Officer of Silvergate and wrote an affidavit, a sworn testimony subject to perjury, in which she detailed the events that led to Silvergate voluntarily winding down their business and returning deposits to their customers.

This affidavit is a bombshell because it confirms speculation that Silvergate was solvent in early 2023 and wasn't shut down because of bad risk management on behalf of the bank's management team, but instead was forced to shutter its doors because the Biden Administration, with strong influence from Senator Elizabeth Warren, forced Silvergate's hand because they didn't like that they were banking digital asset companies.

For those who are a bit fuzzy on the details of the narratives that were flying around Silvergate at the time, I'll jog your memory. FTX was a customer of Silvergate's at the time their Ponzi scheme unraveled. As FTX was blowing up, everyone and their mother was scrambling to get their money out of Silvergate because they assumed that since one of the bank's largest counterparties was going bust, the bank must be in trouble too. A sane decision. Especially considering the history of systemically non-important financial institutions this century.

Unless you were paying close attention during this time, you were likely under the impression that Silvergate was a typical fractionally reserved bank that was experiencing a run that led to its inevitable demise. The media made it seem this way. The regulators made it seem this way. And one pompous short seller made it seem this way. However, nothing could be further from the truth.

Here are the most important parts of the affidavit:

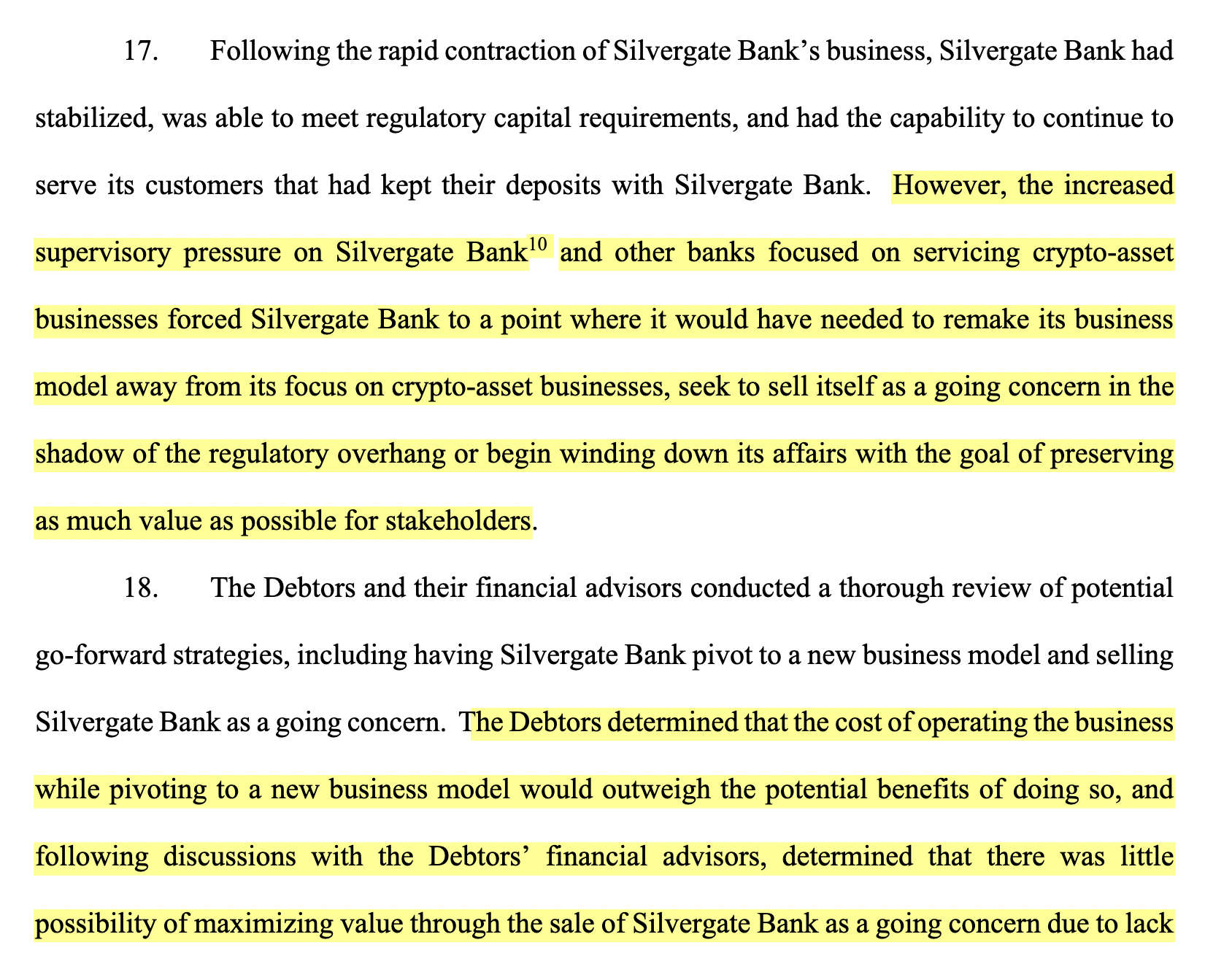

"Silvergate had stabilized, was able to make regulatory capital requirements, and had the capability to continue to serve its customers that had kept their deposits with Silvergate Bank."

Despite this, regulators decided to turn the pressure up and essentially gave Silvergate Bank, and Signature Bank as well, an ultimatum; drastically change your business models immediately by dropping your digital asset customer base or we'll shut you down. There were no hard numbers described in Elaine's testimony, but rumors are that the regulators wanted Silvergate to quickly shrink their exposure to digital asset-related clients to less than 15% of their capital base. At the time, Silvergate's customer base was made up almost entirely of digital asset companies (99.5% to be exact).

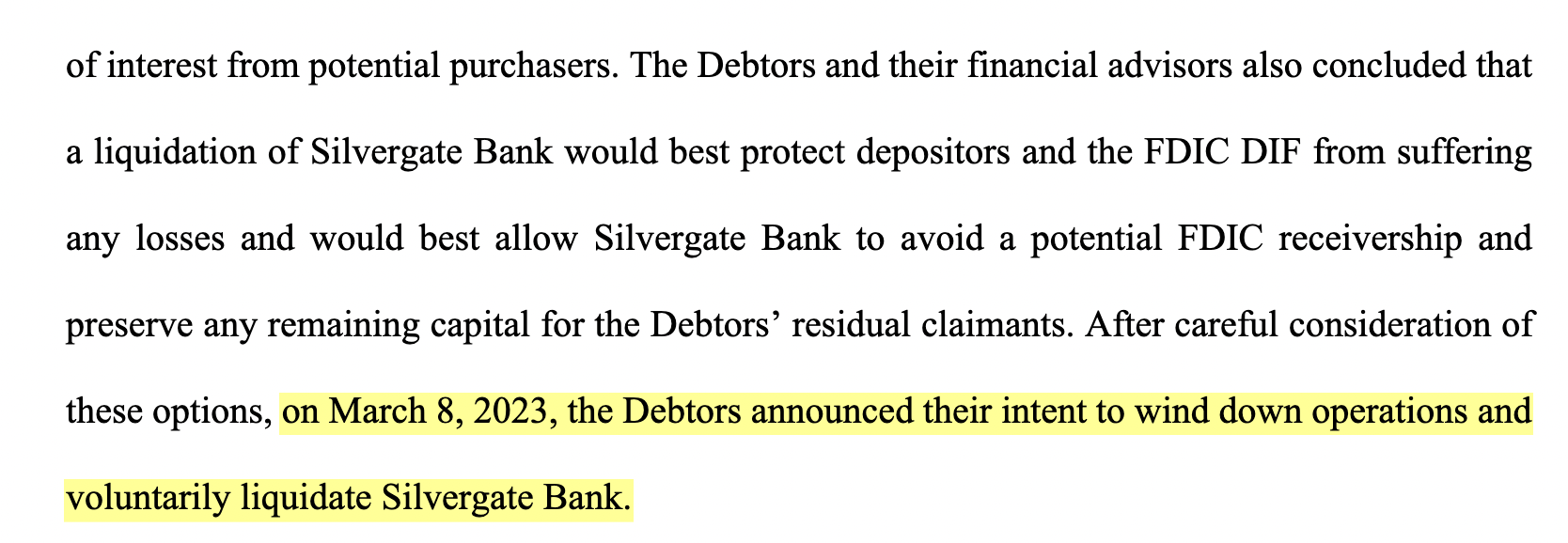

The regulators were asking Silvergate to do something that was quite literally impossible given the circumstances. Faced with an impossible task, on March 8th of 2023 Silvergate decided to voluntarily wind down their operations and return deposits back to their customers.

Let's be very clear here, Silvergate did not lose a single penny of customer deposits due to the run on their bank. Management, understanding the volatile nature of the digital asset markets, designed their risk management and capital allocation strategies in a way that would enable them to return dollars to any customer who requested them. And that's exactly what they did when customers came to request their money. They returned EVERY SINGLE PENNY.

This begs the question, "Why did they essentially force Silvergate to shut down?" They seemed to be running a very responsible operation after all. You'd think the regulators would applaud Silvergate's vigilance in risk management on behalf of their customer base. How many banks would have been able to do the same thing if put in the same situation? Probably not many.

The answer to this question is already well known throughout the industry, but Elaine Hetrick's testimony adds some hard evidence that makes it undeniable; Elizabeth Warren, the SEC, the FDIC and the Federal Reserve have been acting in concert to unconstitutionally and extrajudicially target the bitcoin and broader digital asset industry because they do not believe that it should exist. It is a threat to their power structure. The financial system, as it is designed today, gives those who would like to centrally plan the economy and micromanage the lives of American citizens a ton of power. Bitcoin is a threat to that power and they have to do everything in their power to prevent its proliferation.

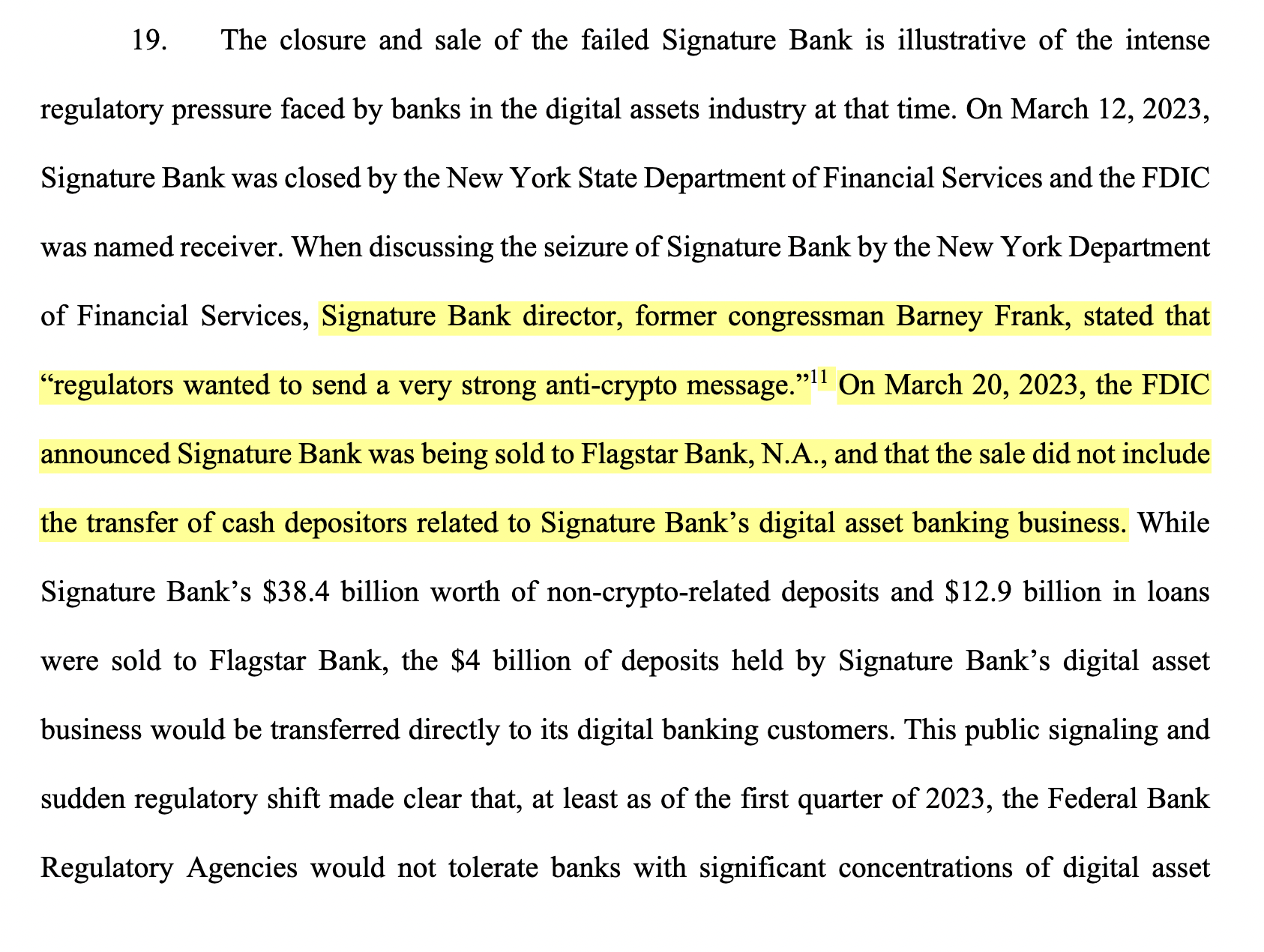

The targeting of the industry was also confirmed by the aftermath of the NYDFS and FDIC uncharacteristically taking Signature Bank behind the woodshed in the evening of Sunday, March 12th, 2023, despite the fact that Barney Frank and others at the bank were convinced they could handle withdraws come market open the next day.

Signature Bank was ultimately sold to Flagstar Bank. However, they were forced to spin out their digital asset-related accounts before doing so.

This public signaling and sudden regulatory shift made clear that, at least as of the first quarter of 2023, the Federal Bank Regulatory Agencies would not tolerate banks with significant concentrations of digital asset customers, ultimately preventing Silvergate Bank from continuing its digital asset focused business model.

Pretty damning if you ask me. Also, very frustrating and most definitely illegal.

Elizabeth Warren and her gaggle of hall monitors across alphabet soup agencies and the Federal Reserve have been on one massive, unconstitutional, power trip for the last four years. They've besmirched bitcoin and those of us working hard to ensure that the United States of America leads the way forward as bitcoin adoption continues at every turn. Good people striving to make the world a better place.

No one is a better example of this than Alan Lane, the former CEO of Silvergate Bank. I consider Alan a friend and feel supremely confident when I say that he is one of the nicest and most thoughtful people I have met in this industry. A man who followed his passion to bring legitimacy and much needed banking services to an industry that the incumbents refused to touch. And he did bring legitimacy. As I explained earlier, Alan and his team understood the volatile nature of the industry and built their firm in a way that took this volatility into account. Silvergate did not fail, they were forced to shut down by Elizabeth Warren and her acolytes at the regulatory agencies.

What's worse, Warren's vendetta against bitcoin and the digital asset industry incited the largest banking crisis this country had seen since 2008. Silvergate and Signature being taken behind the woodshed put everyone on their toes and bank runs started across the country. This led to the failure of First Republic, Silicon Valley Bank and a couple of smaller banks, forced the Fed to step in with their emergency BTFP program, and burdened taxpayers with $40B in FDIC costs that needed to be absorbed as a result. If it weren't for the bailouts things would have gotten completely out of control. All because Elizabeth Warren wants to live in a world in which we are forced to use CBDCs and unable to opt-in to bitcoin.

The euthanasia of Silvergate and Signature are only the tip of the iceberg when it comes to Chokepoint 2.0.

Caitlin Long and Custodia have been in a years long battle with the Federal Reserve to receive a Fed master account so that they can properly serve their customers. For those who are unaware, Custodia is a full-reserve bank that exist to serve bitcoin and digital asset businesses as well as other adjacent businesses like fintechs, banks and funds. Custodia is a chartered bank and special purpose depository institution that has built custody services so that customers can hold bitcoin within their bank accounts alongside their dollar accounts.

Like Silvergate and Signature, Custodia has been singled out and unlawfully denied a master account with the Fed because the Federal Reserve doesn't want a bank like Custodia to exist. Either because they worry about the ramifications of the introduction of a full-reserve bank into a system dominated by fractional-reserve banks or they simply do not want to see bitcoin succeed. If we're being honest, it's probably a combination of the two.

Despite what we, or anyone else, thinks about the potential effect a bank like Custodia could have on the market if it's granted a master account, the Fed's actions are unconstitutional in this case as well. This was made pretty clear (but yet to be determined by a court) in an amicus brief written by Paul Clement on behalf of Custodia earlier this Summer. The Fed is actively undermining the dual-banking system that was set up in this country to enable competition between state chartered banks and the Federal Reserve system.

By arbitrarily singling out banks that bank bitcoin companies and denying them master accounts, the Fed is actively undermining the dual-banking system that has existed for centuries and enables states to experiment.

— Marty Bent (@MartyBent) September 24, 2024

The Fed is acting with authority it doesn't have. https://t.co/sXLGA6OI8B pic.twitter.com/gs9j2tiHri

In the case of Custodia, the Federal Reserve is exhibiting expansive discretionary power that it has never shown before. Custodia is a state chartered special purpose depository institution in the state of Wyoming. Historically, it would be trivial for this type of state chartered bank to get a master account with the Fed. But for whatever reason (we know the reason) the Fed has been denying Custodia their right to this account for a number of years. To the point where Custodia was forced to sue the Federal Reserve and take their case to the courts.

What's interesting about the saga of Custodia and the Fed is that it has forced Custodia's legal team to dig in and highlight where the Fed is overextending its reach and acting arbitrarily. In the amicus brief that was published in July of this year, Paul Clement argues that the way Federal Reserve Bank presidents are chosen is unconstitutional when you take into consideration the fact the these Fed branch presidents are unilaterally undermining state banking laws by denying master accounts.

If they are going to unilaterally undermine state banking laws they need to be appointed by the President or an official acting on behalf of the Executive Branch. Federal Reserve Bank presidents aren't appointed by the President of the United States or any official acting with the authority of the Executive Branch. Instead, they are appointed by their boards, which are controlled by the privately held commercial banks who own them. The Federal Reserve system is clearly acting unconstitutionally when they deny Custodia from being assigned a master account.

The people in power within the federal government and the Federal Reserve system are actively targeting the bitcoin and digital asset industry, acting extrajudicially and making a mockery of the rule of law in the United States. They are completely out of control and it is important that everyone who cares about the future of bitcoin in the United States and the future of the United States more broadly (even if you don't like bitcoin) speaks out and fights against these totalitarians as vehemently as possible. What they are doing is wrong. It's unconstitutional. And it is putting the future of our country at risk.

If the federal government, the regulators and the Federal Reserve do not get out of the way and let law abiding citizens build the businesses they want and associate with businesses they want, those businesses will go elsewhere and the United States will be set back generations as a result.

It's time to put these people in their place and let it be known that freedom will reign supreme in the Land of the Free. Fight!

Final thought...

I promised Parker Lewis that I would do cross fit on Friday morning and I'm using today's final thought as an accountability tool.