We're winning. Embrace it.

This tweet set off a lot of controversy on X this evening. I knew it would when I hit send. Many people are tied to bamboozling narratives that the Ethereum project brought to the world of "decentralized world computer" and "every financial agreement settled via a smart contract". To date, the DeFi meme has led to a colossal amount of capital misallocation that has produced nothing more than Rube Goldberg machines of cross collateralized ponzi machines dependent on a perpetual flow of greater fools who believe that a token for every conceivable use case actually makes any sense. The DeFi protocols that remain (from what I can tell) mainly serve people looking to generate additional yield or leverage on the best performing asset class of the last 15-years. The enabling of degeneracy.

Don't fret, though. The DeFi advocates went back to the drawing board during the bear market and are back this cycle pushing the narrative that this time around the tokenization of "Real World Assets" (RWAs) is what is going to fix the inherent structural issues that existed and continue to exist in the first iteration of DeFi protocols. By tying RWAs to DeFi protocols, users can reap the benefits of more stable collateral coupled with the decentralization and automation of DeFi protocols. These people have obviously not read enough of Gigi's musings.

By injecting RWAs into DeFi protocols you are compounding inefficiencies. Firstly, it is impossible to tie real world assets to blockchains because there is nothing a blockchain can do to enforce contract law in meat space. Secondly, the owners of those RWAs are inheriting the layered protocol risk of the blockchains the DeFi protocols run on. What happens when a smart contract bug enables the Lazarus Group to steal your tokenized real estate or equity shares? Does Kim Jong Un own the cash flows of your rental property and your Coca Cola dividends now? Will the DeFi protocol "roll back the chain" to make things right? If so, you'll quickly learn the lesson that you didn't need a blockchain in the first place.

After years of observation I think I've finally honed in on the core of the problem with DeFi and its advocates; they want to completely ignore and abandon the edifice of finance which has been erected over the course of millennia and build it all back from scratch using tokenized digital assets that shouldn't exist in the first place. They do not solve the problems people think they do. What is desperately needed is a distributed peer-to-peer cash system with a fixed supply that cannot be corrupted by central authorities and ultimately replaces central banks as the issuer and maintainer of the global monetary system.

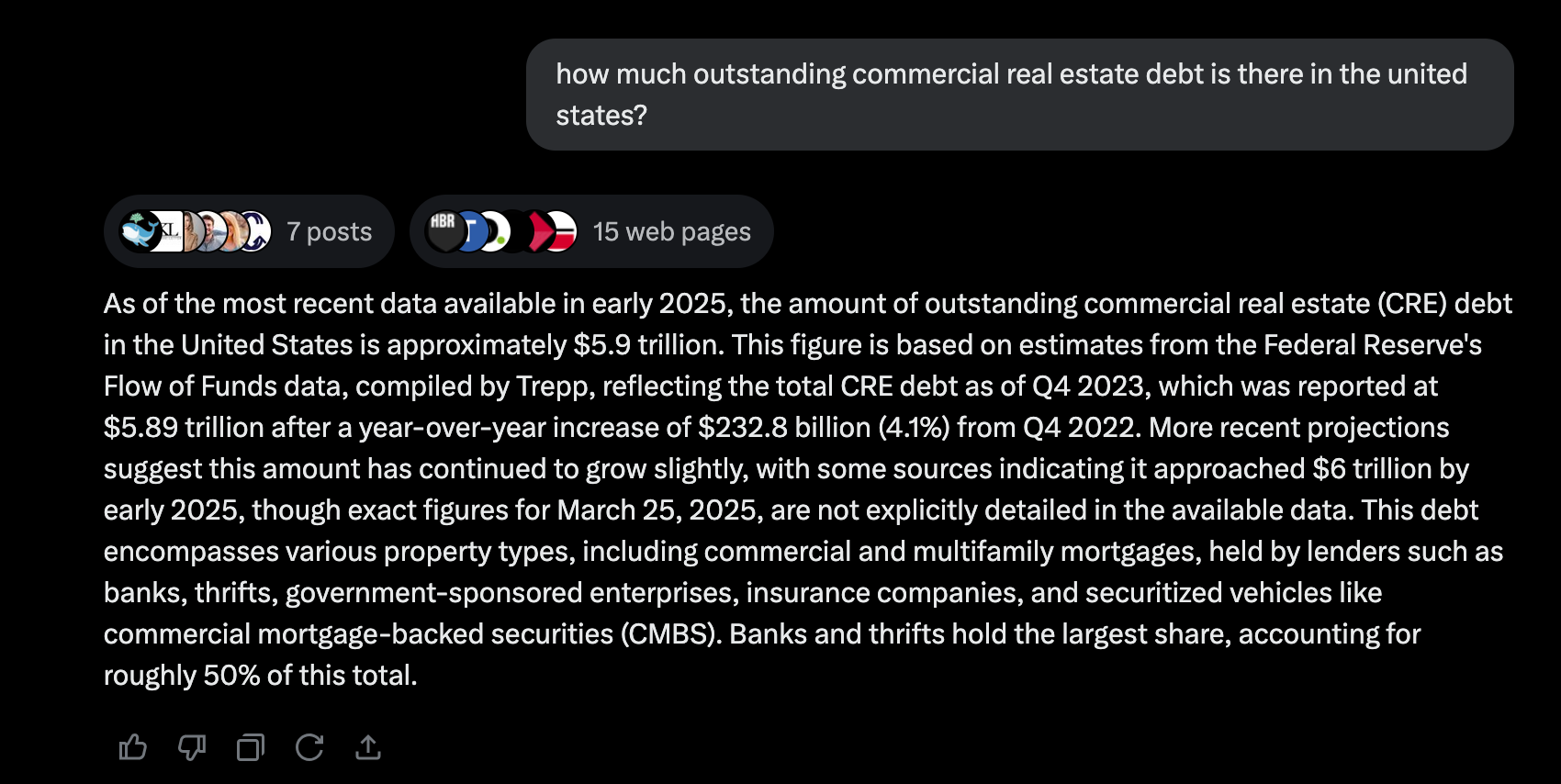

That is what bitcoin brings to the world with and it is a singular product that can have a profound healing effect on a financial system recovering from its addiction to easy money creation. As much as I like the idea of completely ditching the traditional financial world and starting a new one from scratch, it is completely impractical, unproductive and would leave a lot of people destitute. TradFi NEEDS bitcoin, and this is a good thing because it presents a path toward upgrading the traditional financial system with modern tech while also producing the much talked about soft landing for the economy. At least over the course of a couple of decades. Let's put this into perspective by looking at the market for commercial real estate in the United States.

There is currently $5.9 TRILLION of outstanding commercial real estate debt in the United States right now. That is an enormous amount of debt that is using real estate, a consumable good subject to the laws of entropy, as the predominant form of collateral. The combination of the continued squeeze on the middle class and the post-COVID under-utilization of office space makes this debt particularly risky (to me, at least). Instead of trying to recreate this multi-trillion dollar market in the world of DeFi, which is a sub-optimal solution looking for a problem, it makes more sense to me that anyone who is so motivated should aim to begin refinancing this commercial real estate debt and introduce bitcoin as collateral in the process.

In my mind you could refinance this debt in two ways at the moment. The first is the Battery Finance model; the lender recognizes the long-term risk of using real estate as the sole collateral in a credit structure and consciously decides that a portion of the loan proceeds must be allocated to bitcoin with the upside appreciation of the bitcoin shared between the borrower and lender at the end of the loan. In this model, the lender de-risks the capital they're putting up. The real estate value could remain flat or even fall, but the bitcoin makes up for that underperformance on the back end. Enabling them to increase the purchasing power of their capital. On top of this, at the end of the loan term the borrower's equity is preserved and likely increased, also due to bitcoin's appreciation, and they are a new bitcoin holder.

The second scenario is a preexisting bitcoiner who wishes to bring bitcoin to the financing table as collateral from the jump to lower their cost of capital and diversify their own collateral in the loan structure. They are able to tap into the value of their bitcoin to acquire a line of credit and an asset to better their lives and if they continue to be productive and pay back their loan on time and in full, they get to keep their bitcoin when the loan comes to term. A win-win.

All of this can be done in a way that preserves the "don't trust, verify" ethos as well via multi-sig escrow where the borrower, the lender and a neutral third party hold three keys in a 2-of-3 quorum. Heck, you can even add smart contracting functionality to the deal in the form of timelocks via Miniscript. We're already beginning to see this emerge via the insurance product that Anchorwatch has brought to market. A perfect example of the bitcoinization of finance, which is often wrongly framed as the financialization of bitcoin. Anchorwatch is bringing bitcoin native tech to the insurance industry that gives the end-user the ability to make sure their bitcoin isn't being misappropriated because they hold keys in the quorum throughout the duration of the policy.

This will be applied to every financial product that is bitcoinized eventually because it will be demanded by the market. Out of the gate it likely won't be adopted by every institution, some will take risk with the bitcoin, lose it, and the market will re-learn the lesson of "don't trust, verify", especially when you don't need to in a world in which bitcoin script is available to build on.

All of this will also serve to create more stability in the price fluctuations of bitcoin. If products like these are brought to market and widely adopted, the bitcoin price will march higher, and with it it's market cap. A higher market cap with less volatility will make more people comfortable spending their bitcoin, at which point many will choose to leverage the permissionless stack being built on top of the protocol; lightning, liquid, Ark, Chaumian mints, etc.

The bitcoinization of finance doesn't prevent the permissionless innovation that is already happening on bitcoin, it likely accelerates it. And any bitcoiner with any legitimate sense of risk-management won't be aping their whole stack into bitcoin-collateralized products to take out lines of credit. The wise move would be to use a small portion of your bitcoin holdings to reap the benefits of these products, increase the quality of your life by acquiring other assets you desire and/or need, and continue to use the rest of your holdings in a self-sovereign fashion.

Those who believe bitcoin is being co-opted because it is being recognized as a superior collateral asset in the world of traditional finance have a loser's mindset. Bitcoin is being chosen because it is superior. That is a positive signal that should be embraced. Bitcoin being embraced does not mean that Wall Street gets to hoover up all of the bitcoin and prevent their clients from reaping the benefits of bitcoin's native properties. The superior products that leverage bitcoin's native properties already exist and will continue to proliferate as market participants demand them.

Compared to the world of degenerate nonsensical DeFi, the bitcoinization of finance makes a lot more sense, has a clearer path to implementation and clear benefits that make all parties involved better off.

Bitcoin replacing real estate, dollars, treasuries and other forms of inferior collateral in credit products is a sign that bitcoin is successfully demonetizing all of those assets and shifting control toward the holders of bitcoin. That's winning.

This letter was inspired by the reaction to the tweet above, which was inspired by a conversation I had with Pierre Rochard on the TFTC podcast earlier today. That episode should be live one hour after this hits your inbox. You should check it out.

As Peruvian Bull expertly outlined on our podcast last month, we're witnessing the endgame of unsustainable government debt. The data is sobering—54 out of 55 countries that exceeded 120% debt-to-GDP have defaulted through currency debasement, hyperinflation or depression. With U.S. debt now at 132% of GDP, we've crossed what Peruvian Bull calls "the monetary event horizon" with $10 trillion in debt needing rollover in 2024 alone.

"They're trapped in this black hole of their own design. There's no magic button they can press that will get them out of this." – Peruvian Bull

This debt trap creates what Peruvian so humbly called "the Peruvian Bull debt paradox" – higher interest rates increase government borrowing costs, forcing more debt issuance, which pushes yields higher, necessitating even more borrowing. It's a vicious cycle with only one escape: money printing. While GameStop recognizes this reality by buying Bitcoin for its treasury, the implications go far beyond any single company. As central banks face this mathematical inevitability, the resulting "infinite liquidity" environment makes Bitcoin's scarcity not just valuable but necessary.

Check out the full podcast here for more on gold market shortages, Ryan Cohen meeting with Michael Saylor, and why traditional investment markets are more manipulated than you think.

Google's Gemini 2.5: New AI Model Debuts - via Google

Trump Signs Treasury Modernization Order - Via X

Tesla Robotaxi Service Launch Scheduled for Austin in June - Via X

GameStop's Bitcoin Investment Policy Update - Via X

ICYMI Fold opened the waiting list for the new Bitcoin Rewards Credit Card. Fold cardholders will get unlimited 2% cash back in sats.

Get on the waiting list now before it fills up!

$200k worth of prizes are up for grabs.

Ten31, the largest bitcoin-focused investor, has deployed $150M across 30+ companies through three funds. I am a Managing Partner at Ten31 and am very proud of the work we are doing. Learn more at ten31.vc/funds.

Final thought...

It's been two years since my dad passed. He's the reason this newsletter and TFTC as a company exists. I like to think he enjoyed a refreshing black and tan in heaven today.

Love you, Dad.

Get this newsletter sent to your inbox daily: https://www.tftc.io/bitcoin-brief/

Subscribe to our YouTube channels and follow us on Nostr and X:

|