How the orange coin fixes the broken global reserve system.

Triffin’s Dilemma is the fatal flaw in the Bretton Woods system- a paradox that eventually destroys every reserve currency.

But what if it could be solved?

The Bretton Woods system was established in 1944 as an international monetary system designed to provide stability to the global economy after the ravages of World War II. Under this system, the U.S. dollar was pegged to gold, and other major currencies were pegged to the dollar. The U.S. dollar became the world's primary reserve currency, and member countries agreed to maintain exchange rates within specified bands by intervening in the foreign exchange market. The International Monetary Fund (IMF) and the World Bank were also created as part of the Bretton Woods framework to facilitate international economic cooperation and development.

The structure of the system was designed to directly benefit the United States- apart from the obvious instatement of the Dollar as the global reserve currency, the low pegged price of gold ($35/oz) meant that gold was severely undervalued.

The emergence of a gold-dollar system was ostensibly driven by insufficient growth in the global gold supply to support expanding world trade and output- the choice of post-war currency parities, which kept the real price of gold low and limited gold production, contributed to this shortage. Additionally, the USSR and South Africa, major gold suppliers, were deemed unreliable.

(In reality, there was no shortage of actual gold- there is always enough reserves to satisfy demand for trade, the question is a matter of price. At which price will gold have to be in order for global trade to be settled? The answer was and is certainly much higher than current prices.)

To bridge the gap between the demand and supply of global reserves, dollars became more and more prominent, generated through the accumulation of official short-term claims on the United States starting in the early 1950s. In practical terms, this meant that the US was consistently running balance of payments deficits in official settlements, accruing liabilities to foreign officials without a corresponding increase in assets like gold.

The United States was running current account deficits, which essentially means we were exporting more dollars than we were importing. These excess dollars were showing up in the global system in a multitude of ways- as Eurodollar bank deposits, in dollar swap and currency trade, and as excess dollar reserves at foreign central banks. Corporations and governments who accumulated these surpluses by trading with us now had cash on hand which they promptly reinvested back into the domestic financial system, mainly in the form of debt liabilities such as U.S. Treasuries.

The current account can be broken down into several subcategories which can be seen here:

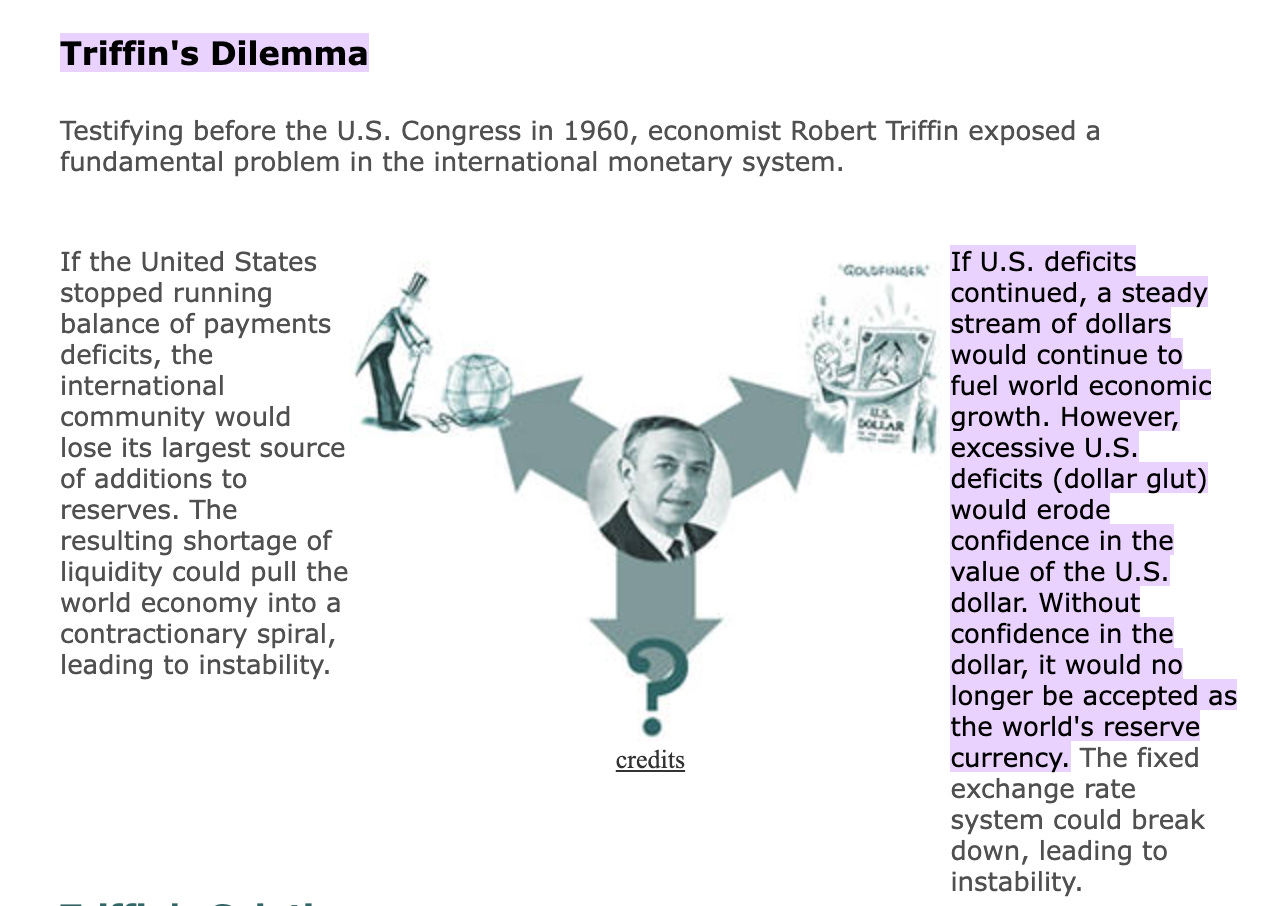

In 1960, a Belgian economist by the name of Robert Triffin gave a presentation in front of Congress on what he saw as a fatal flaw in the Bretton Woods global monetary system. The flaw he presented came to be known as the Triffin Dilemma or the Triffin Paradox, and it would, he asserted, destroy Bretton Woods in a long enough timeframe. He had also predicted this contraction in global reserves would lead to a worldwide deflationary crisis, which did not come to pass- instead manifesting as a wave of inflation that crashed over the U.S. and much of the world economies.

The Dilemma can be easily summarized as follows.

The Dollar is the world reserve currency. This meant it would be used in international trade, as central bank forex reserves, to settle financial transactions, and to borrow and lend dollar loans offshore (Eurodollar). However, the rest of the world lacked a crucial factor- the ability to generate dollars.

America faces a dilemma- do we meet this demand or not? If we do not print, then an insufficiency of global reserves emerges. Trade begins to grind to a halt, central banks cannot defend their currency in the forex market, and banks cannot service dollar loans. This can cause system-wide defaults and a deflationary crisis that spreads like a viral contagion from one nation to another.

To prevent this we take on the other side of the dilemma- the U.S. needs to run persistent current account deficits, sending out more dollars to the global system on net than it takes in, to fund all these needs. In the long run, however, this means the U.S. will print more dollars than is otherwise justified by our reserve ratio to gold. This ratio will go lower and lower, until there is such an overhang of dollars that a global run on the U.S. dollar itself commences. The excess surpluses of dollars all flow back for gold, until the gold runs out.

That’s essentially what happened.

As the world began to globalize, and nominal GDP growth outside the U.S. began to accelerate, more and more dollars built up outside the domestic financial system. In 1965, French President Charles de Gaulle did the math and realized that the U.S. had issued many more dollars than was justified by the $35/oz reserve ratio and began redeeming dollars for gold, as he was entitled to under Bretton Woods. He was not alone; other nations soon followed suit. A run on American gold reserves began as thousands of metric tons of gold began flowing out of the U.S. (see above).

"The German withdrawal from the Bretton Woods agreement sparked panic and a currency crisis. By the end of June 1971, $22 billion in assets had left the US. Later, in July 1971, Switzerland redeemed $50 million for gold and one month later in August, pulled its Swiss Franc from the Bretton Woods agreement. At the same time, France redeemed $191 million for gold by sending a French battleship to New York to take delivery of the gold from the Federal Reserve and to bring back to France".

De Gaulle had hammered in the nail to the dollar coffin that was Triffin’s so-called Dilemma. He had called the Americans’ bluff, and forced the U.S. to engage in a massive drain in reserves- even calling for a reinstatement of the gold standard system that had functioned before. In doing so, he was removing what his finance minister Valéry Giscard d’Estaing had called “The Exorbitant Privilege”- the ability of the U.S. to run balance of payment deficits and fiscal deficits and force the global system to absorb the fallout. Other nations must stay fiscally and monetarily responsible, and keep their currency pegged to the dollar within the narrow exchange rate- but the U.S. had no need to do so. It received real goods for a currency it could print, feeding the hungry and growing U.S. imperial machine. Building our Empire.

A New York Times article published in February of 1965 lays it out;

“Perhaps never before had a chief of state launched such an open assault on the monetary power of a friendly nation. Nor had anyone of such stature made so sweeping a criticism of the international monetary system since its founding in 1944. There was Charles de Gaulle last week proclaiming that the primacy of the dollar in international dealings was finished, calling for an eventual return to the gold standard —which the world’s nations scrapped 50 years ago — and practically inviting other countries to follow France’s lead and cash in their dollars for gold. It was a particularly nettling irritant just as the U.S. was deeply involved in making some hard decisions about its monetary policy.”

The U.S. had started the system with a huge hoard of gold- approximately 50% of all above-ground gold reserves were held by the Americans. However, this run on the dollar began draining this treasure chest until this figure had fallen by more than half. Most other countries in the Bretton Woods system began following France’s lead.

The crisis reached a head in August 1971 when Nixon famously decided to close the gold window, freezing the ability of foreign central banks and governments to redeem dollars for gold. In doing so, he cut the last link between the paper dollar and the underlying real money- the ability of citizens to demand gold for dollars had already been banned in 1933 under Roosevelt. Of course, Nixon had promised that this break from the gold standard was temporary, and once a solution was found we would return to sound money. However, this never happened.

It has been long debated whether we could get off this new (euro)dollar standard- if any single usurper could overtake the United States in global trade and political influence and be able to enforce a new global reserve currency. In general, any new global reserve currency must meet a laundry list of requirements, it must have structural advantages over the U.S. dollar, and most importantly- it must stand up to Triffin’s dilemma. At least for as long as the Dollar did (preferably longer).

(Side note- Triffin’s Dilemma still applies, but now the new reserve asset is U.S. Treasuries, not gold. The U.S. has been exporting USTs for decades and they have built up on the balance sheets of overseas financial institutions. Foreign Central Banks are no longer buying USTs on net.)

The current consensus among macroeconomists is the TINA doctrine- There Is No Alternative. Russia is a commodity exporter (current account surplus), which would need to be switched into deficits to be a reserve currency. China has a closed capital account. India does not have a deep enough bond market. South Africa is politically unstable. None of the above have good enough rule of law. As Brent Johnson points out, the U.S. has deep and liquid bond markets, rule of law, a sophisticated financial and monetary system, and a gargantuan military to enforce the dollar system- basically everything one could want. This is the system we are stuck in.

The list of requirements for a reserve currency are as follows:

Bitcoin is still in its nascent stage of growth as a currency. As of November 11th 2023, the market cap stands at approximately $720B, and BTC trades for $36,800. Volatility is still elevated, as the size of the market means that relatively small amounts of money can move price action disproportionately compared to to other markets.

So it “fails” the stability test. For now.

Is Bitcoin safe? It is as safe as your own ability to hold your keys! If you hold Bitcoin non-custodially and maintain secure ownership over your seed phrase, then it certainly is safe. Arguably it is much safer than almost anything else- similar to physical gold, it is a bearer asset and a true digital commodity. It can’t be easily stolen or censored. Dollar assets, as we saw with Russia’s ban from the SWIFT network, can be frozen or seized. Dollar transactions can be blacklisted by the Treasury’s OFAC (Office of Foreign Asset Control) division. You can be censored. You are only safe insofar as you are not in opposition to U.S. government interests.

Bitcoin is the best store of value ever invented- even superior to gold. The yellow metal inflates its supply at approximately 2% per year, and no one knows the true quantity of gold that exists. BTC instead has an issuance schedule that is mathematically determined and enforced by the structure of the network (node and miner consensus), guaranteeing that 21M (or infinitely close to it) is the maximum amount of Bitcoin that can ever be mined. As for medium of exchange, it also fulfills this role as it is very easy to transfer and confirming transactions on the base layer takes around 30 minutes- but this is much faster on Lightning. The Lightning Network is the scaling solution that BTC so desperately needs to be a bona fide medium of exchange for daily life in a modern digital economy.

As for trust, Bitcoin succeeds here as well, as it uses military grade cryptography and miner energy expenditure to secure the blockchain. A form of reverse prisoner’s dilemma ensures that no single miner or node really has an incentive to lie about the validity of transactions, as creating false blocks and transactions requires one to get exponentially more lucky as time goes on, and spend energy (money) doing so. For many complex and technical reasons, attacking the network consistently just isn’t that feasible.

Deep and liquid markets- again we are not here yet, but as BTC gains global adoption depth and liquidity will follow, dampening volatility and bringing more and more capital into the ecosystem. Similar to the flywheel effect with software companies, more and more users (and nation states) adopting Bitcoin means price moves up, volatility dampens, and adoption accelerates in positive feedback loops.

The paradox rests on several foundational points, the main one being a central issuer working in a global monetary system that has demand for its currency. However, Bitcoin is NOT centrally issued. There exists no borders to Bitcoin, no single node of issuance, and orbiting nodes with demand. Any miner in the entire network can be chosen for the next block reward.

Thus, it can’t even be applied here. A neutral reserve currency, non-centrally issued, free-floating, fully reserved, was the standard for centuries prior to the fiat system. Triffin himself imagined a solution to the problem- however, his idea was that of the SDR (Special Drawing Right), a unit of reserve issued by the IMF that was based on a basket of other currencies. SDRs do nothing to mitigate the problems of inflation and fiat debasement, and furthermore would be incredibly hard to manage. Imagine redeeming SDRs for the base currencies, and having to go individually to each country to collect the money.

With a neutral reserve currency, individual nations’ current account deficits or surpluses balance out. If a country spends more than it earns from the global system on net, it eventually is forced to start earning (producing) again. And if the inverse occurs, a nation produces excessive amounts, it builds up surplus savings that can be used for consumption, sending these reserve balances back out into the system. The entire global economy would thus be self-balancing.

The rush from the current system into Bitcoin would solve all the other qualms that macroeconomists have about the orange coin as well- depth and liquid markets would develop, the price would move exponentially higher, adoption would spread as dozens and then over a hundred nations adopt digital gold and begin using and demanding it in international trade and finance.

This was originally posted on Dollar Endgame.